3 Options for Rental Car Insurance in Europe

Driving abroad in Europe

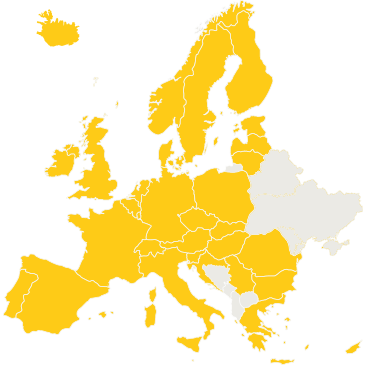

As an AA car insurance policyholder, you can drive anywhere in the EU, and in several other European countries, and get the same level of cover you have in the UK for up to 90 days during the 12 months of your policy.

Your car insurance is valid in the following countries:

- Andorra

- Austria

- Belgium

- Bosnia and Herzegovina

- Bulgaria

- Croatia

- Cyprus

- Czech Republic

- Denmark

- Estonia

- Finland

- France

- Gibraltar

- Germany

- Greece

- Hungary

- Iceland

- Italy

- Latvia

- Liechtenstien

- Lithuania

- Luxembourg

- Malta

- Monaco

- Netherlands

- Norway

- Poland

- Portugal

- Romania

- San Marino

- Serbia

- Slovakia

- Slovenia

- Spain

- Sweden

- Switzerland

- Vatican City

Documents for driving abroad in Europe

From 2 August 2021 a Green Card (or International Motor Insurance Card) is no longer required for travel in the European Economic Area, which includes all the European Union countries plus Iceland, Liechtenstein and Norway. You also don’t need a Green Card for Andorra, Bosnia and Herzegovina, Serbia and Switzerland.

You do still need to take:

- your Certificate of Motor Insurance

- the log book (V5C) for the vehicle

- your driving licence.

The Republic of Ireland is within the territorial limit of our car insurance, so policyholders get the same level as cover there as they do in the UK all year round.

Longer trips and business travel abroad

Let us know in advance if you’re planning to take your car to Europe for more than 90 days and want the same level of cover as you have in the UK. If this is acceptable, you may have to pay a fee for the extended cover.

If the same level of cover isn’t available, or you don’t want the same cover as you have in the UK, you’ll only have the minimum insurance cover needed by law in the country you’re visiting after the 90 day period has ended.

Please also tell us if you’re planning to use your car for business travel abroad.

Lines are open Monday to Friday 8am to 8pm, Saturday 9am to 5pm.

Travelling further afield

Do tell us if you want to take your car to a country that isn’t listed above.

If the same level of cover as you have in the UK is available, you could have to pay a fee for this and you’ll need a Green Card too.

Alternatively, only the minimum insurance cover needed by law in the country you’re visiting may be available. Again, you may have to pay a fee for this, and you’ll need a Green Card.

There may be some countries where cover is not available.

- Call us for advice on 0344 412 4684

Government advice

Breakdown cover

For peace of mind, AA European Breakdown Cover has a 24-hour English-speaking phone helpline for when you’re driving abroad.

3 Options for Rental Car Insurance in Europe

Many or all of the products featured here are from our partners who compensate us. This may influence which products we write about and where and how the product appears on a page. However, this does not influence our evaluations. Our opinions are our own. Here is a list of our partners and here’s how we make money.

Renting a car for your vacation in Europe is just the first step in planning a road trip. Now you have to make some key decisions: whether to buy rental car insurance and, if so, whether to purchase a specialty policy or get insurance at the car rental counter.

If you are traveling to Europe and renting a car, you have three main insurance options for your trip.

1. Free coverage through your credit card

Your first call should be to your car insurance carrier or agent, although most U.S. personal auto insurance policies will not cover you in Europe.

However, your credit card might offer coverage for free. In that case you might not need to buy rental car insurance at all.

To find out what benefits you have, call your credit card company and ask about insurance coverage for European car rentals. Major credit card companies typically offer insurance for damage to the vehicle up to a certain amount, such as $50,000, plus other expenses such as towing. This may be referred to as collision damage waiver (CDW) or loss damage waiver (LDW).

Note this insurance will probably not cover the cost of injuries incurred in an accident or other liability. If you have significant assets, you should check with your insurance agent about umbrella liability coverage, which may cover you abroad.

If you opt to go with your credit card insurance instead of purchasing other coverage, be sure you are listed as the driver and pay for the car rental on the card that offers the coverage. You will also have to decline the rental car agency’s damage waiver coverage. If you fail to do either of these things, your credit card will not offer you any protection.

Some credit cards exclude coverage for certain types of luxury cars and won’t cover you in certain countries, such as Ireland and Italy. And be aware that if you’re in an accident, the rental car company will charge your card for the damages while your claim is being processed by your credit card company. You may have to wait for reimbursement.

2. Stand-alone insurance policies

If your credit card does not provide coverage, you can buy insurance specifically for one trip or for an extended time frame.

One option is trip insurance , which can prove coverage for car rentals as well as trip cancellation and trip interruption.

Trip insurance comparison website InsureMyTrip.com allows you to get quotes from multiple travel insurance companies. Quotes for travel insurance for one week in Britain — including car rental insurance, trip cancellation and trip interruption — range from $104 for a policy through HTH Worldwide to $240 through Allianz Global Assistance .

But if you are just looking for car rental insurance, you can find even lower rates through InsureMyRentalCar.com . Launched last year in the UK, Insure My Rental Car currently sells damage waiver insurance with up to $100,000 in coverage to consumers in all states except Alaska, Florida, Hawaii, Massachusetts and Vermont.

The cost: $17.50 for up to 31 days or $93.99 for an annual policy. Coverage can be purchased from six months to one day in advance and covers your rental car use both at home or overseas.

“We’re trying to change the way people shop for rental car insurance, and give you a better deal,” says CEO Ernesto Suarez.

A survey for Insure My Rental Car conducted by market research firm YouGov found that buying insurance at the car rental counter can be expensive, adding nearly 50% to the cost of the rental in some cases. For example, renting a compact family car for a week in August in England costs about $467, plus $216 for CDW insurance. That same vehicle in Amsterdam would cost $283 for the rental, plus about $108 for insurance at the car counter.

The low cost for protection through Insure My Rental Car makes it an appealing option.

3. Buying at the rental car counter

It’s no fun to travel across the globe only to show up at a rental car counter and feel pressured into buying insurance. While this is generally the most expensive option, it might be the best choice for adequate coverage and peace of mind if you haven’t bought another policy or if you’re unsure about your credit card benefits.

Also, you may be uncomfortable relying on credit card coverage because damage charges will end up on your statement, leaving you to foot the bill temporarily and perhaps worry about being reimbursed by the credit card company.

“While the insurance is expensive, taking the coverage means you can sleep at night, as you don’t want issues in a foreign country,” says Neil Adams, president of car rental consulting firm Abrams Consulting Group in Purchase, New York.

While buying at the rental car counter is always an option, using credit card benefits or buying a policy online ahead of time will save you time and money. With those options, you’ll hit the road faster with more cash in hand.

Driving in Europe

A driving holiday in Europe is a great way to see lots of interesting sights during your annual family summer trip, but make sure you’re prepared before you set off

European driving holidays give you plenty of freedom, especially if you take your own car instead of hiring one. Using your own car to journey across Europe means you’ll save money and time, plus you’ll avoid all the confusion around how to hire a car abroad.

But driving holidays can sometimes be stressful. Driving laws and rules differ from country to country, and dealing with an accident has added issues including language barriers.

Before you head off on your driving holiday, make sure you have the right car insurance and that you know exactly what you’re covered against.

Read on to find out more.

Green Cards

The UK government has confirmed that Green Cards are no longer required to drive in:

- Countries in the European Union (EU)

- Countries in the European Economic Area (EEA)

- Andorra

- Bosnia & Herzegovina

- Serbia

- Switzerland

We don’t supply Green Cards for any other country. Essential tier customers will need extra cover to drive abroad.

Does your car insurance cover you for driving in Europe?

Driving your own car in the European Union (EU) means you need to make sure you have the right car insurance. Before you go through the tunnel or get on a ferry, make sure you check with your insurer that you have the right type of cover for your trip.

Cover varies, so while some insurers include European cover as standard many may ask you to add it to your policy.

If you aren’t covered and are involved in an accident abroad, you could be forced to pay a large amount – not only to repair damage to your vehicle and others, but to get your car home too.

If your car insurance does include European cover as standard, it’s important to make sure that you have the right level of cover for your trip. For example, some policies may not cover you for the duration of your holiday, or may not cover your car while it’s being transported.

Check the terms and conditions of your policy carefully, and get in touch with your insurer if there’s anything you’re unsure of.

Car insurance with European cover

Excluding Essential tier, Admiral Car Insurance comes with 90-day European cover as standard. All named drivers on your policy benefit from the cover but you must remember to take the certificate with you on your trip.

Your European cover is valid for the following countries: Andorra, Austria, Belgium, Bosnia & Herzegovina, Bulgaria, Croatia, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Ireland, Italy, Latvia, Liechtenstein, Lithuania, Luxembourg, Malta, Netherlands, Norway, Poland, Portugal, Republic of Cyprus, Romania, Serbia, Slovak Republic, Slovenia, Spain, Sweden, and Switzerland

Your International Motor Insurance Certificate will cover you up to a maximum of 90 days in any one year. If you do wish to exceed the 90 days, please call our customer services team.

Take a look at your policy book for more information on driving your car abroad.

Driving laws in Europe

European countries each have their own driving laws and many European countries ask you to carry extra equipment when driving on their roads.

Don’t be tempted to have a small drink and get behind the wheel, as most European countries have stricter drink-driving laws than the UK. Check European blood alcohol content drink driving limits here.

Like in the UK, using your mobile while driving is illegal in most European countries. If you need to use your phone’s satnav system while driving, make sure it’s attached to your windscreen and not in your hands.

Speed cameras are more and more common throughout Europe and in many countries the police can demand instant payment of a speeding fine.

Follow the government’s advice for driving abroad and make sure you plan your route in advance so you can prepare for all the different requirements of the countries you’re driving in or through.

What do I need to drive in Europe?

In some countries you may be legally required to carry a number of safety accessories:

- A red triangle

- A reflective vest

- A first aid kid

- Spare bulbs

Until recently, you had to attach a GB sticker to your car, unless it has registration plates showing the EU flag and GB logo. As of 28 September 2021, British motorists driving outside the UK must remove old-style GB stickers or cover them up. Instead, you should display a UK sticker or have the UK identifier on your number plate.

If you’re driving in winter in Europe, some countries insist on snow chains and winter tyres. Holding up traffic because your car isn’t equipped with these in severe weather could earn you a fine.

Important documentation to take when driving in Europe

Make sure the following documents are up-to-date and keep them with you just in case the police ask to see them:

- Certificate of Motor Insurance

- A valid full driving licence

- Vehicle registration document: If you’re taking your own vehicle, this is your V5C vehicle log book. If you don’t have this because the car is leased or hired, the only legal alternative is the Vehicle on Hire Certificate VE103, available from the British Vehicle Rental and Leasing Association (BVRLA)

- Your passport: for some countries in mainland Europe but not in the EU (for example, Belarus) you might also need an International Driving Permit (IDP). In most EU countries, your UK driving licence will be sufficient. Some countries in mainland Europe require a Visa too

- An Agreed Statement of Facts on Motor Vehicle Accident

The Agreed Statement of Facts on Motor Vehicle Accident

This is a form all drivers in Europe should keep in their car in case of an accident. It’s a good idea to print one before you travel, and keep it with your other documents.

The form goes by different names in different European countries; it is known as the Constat Amiable in France, the CIA in Italy and the DAA in Spain. The most important thing to know is that the form will be in the language of the country you are in.

If you are involved in an incident with a third party driver while driving in Europe they will present you with the form; it is split into two sections and each driver involved is expected to complete it with their version of events.

The English language form you take with you is for translation purposes only. You don’t need to fill this in – it’s just there to help you understand each section of the form the third party will give you

If you sign anywhere on the report form without ticking any of the boxes in section 12 you are effectively agreeing to the other driver’s version of events. It is a legally binding document and cannot be disputed once signed, so make sure you’re clear on what you’re filling in.

It is essential to add your own version of events by ticking boxes in section 12 or at least providing a comment in English and a diagram in section 13.

Be aware in some countries the Agreed Statement of Facts on Motor Vehicle Accident can be overridden by the police if they attend the accident.

The form has a front page and two carbon copies on the back. In the event of an accident you will need to tear off one of the carbon copies to send to your insurer.

To print off a copy to take with you click here.

Details to get if you’re in an accident

If you’re involved in an accident while driving in Europe, the procedure for collecting details is the same as here in the UK.

Always get the vehicle registration so we can trace the third party insurer, and get details of the driver involved too.

While a lot of this is covered by the Agreed Statement of Facts on Motor Vehicle Accident, some of the following won’t be, so before leaving the scene make sure you have:

- The other driver’s contact details, such as name, address and phone number

- Their insurance details including name of company and policy number

- A copy of the Agreed Statement of Facts on Motor Vehicle Accident

If your crash involves a lorry then make sure you take the registration of the cab and the trailer. The cab and trailer parts of the lorry have different vehicle registrations. It’s essential you note the registration details of the cab so we can trace the lorry’s insurer but it’s always better to get both

Do the same for anything being towed, including caravans and trailer tents.

Get as much information as possible to provide to your insurer, including:

- Photos – try to get pictures of both vehicles, registration of the third party’s vehicle, damage to the vehicles

- If the police or emergency services attend the scene make sure you get their contact details

Be aware in some countries you will be required to pay for attendance by emergency services up front.

Your insurer may also want to see your travel documents in the event you need to make a claim, including tickets and proof of travel.

How to stay safe when driving abroad

The ways to stay safe while driving abroad are largely the same as when you’re driving in the UK. However, there are some safety issues to be aware of while driving abroad.

‘Highway pirates’

Foreign cars in Europe have been targeted by criminals who force them to pull over by pretending that their car is damaged, or by pretending to be traffic police.

If another driver signals for you to stop, make sure you only do so if you’re in a well-lit, public area. If a driver asks to see any of your possessions, make sure you see their ID first.

Theft or other incidents

A handbag, camera or laptop on display will be just as tempting to criminals abroad as it would in the UK.

Keep it hidden, and if you’re unsure about security where you’re going, you can check on advice from the Foreign Office. If you have an emergency other than a breakdown (such as an accident), you can call the 112 number which works in all the EU member states

Emergency cash

Make sure you carry cash for each country you’re visiting. If you’re being adventurous and exploring off the beaten track, any shops or petrol stations you do find, may not accept credit or debit cards.

European Travel Insurance

While the right car insurance will protect your vehicle while you’re on the continent, you and your family should also consider taking out European Travel Insurance before you set off to protect you against things like lost luggage, cancellations and delays and emergency medical treatment.

If there’s a no-deal Brexit, your Global Health Insurance Card (GHIC) will no longer be valid, so taking out travel insurance will be even more important to make sure you’re covered for any necessary medical treatment.

Source https://www.theaa.com/car-insurance/advice/driving-abroad-in-europe

Source https://www.nerdwallet.com/article/credit-cards/rental-car-insurance-quotes-europe

Source https://www.admiral.com/magazine/guides/motor/driving-in-europe